As Africa continues to make strides in the adoption of new technology, with more mobile, online and credit options available, economies and spending are on the rise as well. Going cashless is safer, more secure and opens up new spending opportunities for Africans of many nations.

Mobile opportunity

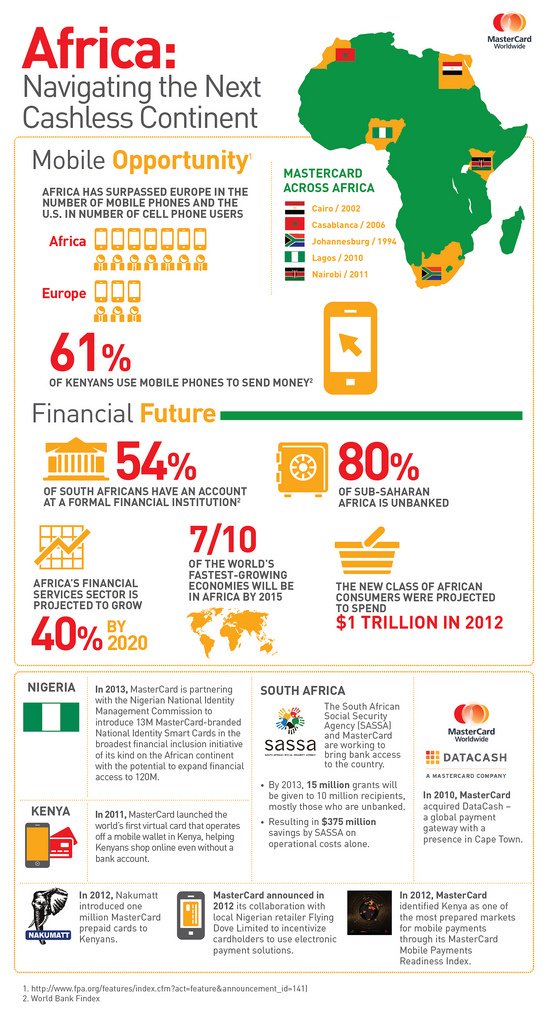

The “Mobile Continent” has certainly been living up to its name, with mobile and card-based payment options overtaking cash-based purchasing by a large margin. The recent mobile revolution has spread phone access far and wide across Africa, and the continent has surpassed not only the number of mobile phones in use than of those in Europe, but the number of cell phone in the U.S. as well.

This widespread access to mobile technology is resulting in a huge upswing in mobile payments. For example, it’s estimated now that 61 percent of Kenyans use mobile phones to send money.

MasterCard and Africa’s Electronic Payment Revolution

Credit card giant MasterCard has been working to bring cashless technology to the continent for more than two decades. Beginning in 1994, the card became available in Johannesburg, followed by Cairo and Casablanca in the 2000s and Lagos and Nairobi in 2010 and 2011. Cashless opportunities aren’t limited to physical credit cards anymore, either. MasterCard launched the world’s first “virtual wallet” in Kenya in 2011, opening the possibility of online shopping, even for those without a bank account.

Indeed, MasterCard has been making its mark across the continent, bringing both credit card and virtual payment options to countries across Africa. Recently, the company has begun partnering with retailers like Flying Dove Limited. After identifying Kenya as one of the markets most ready for mobile payments, they also rolled out one million prepaid cards in Kenya in 2012.

In 2013, MasterCard partnered with the Nigerian National Identity Management Commission to introduce 13 million smart cards in the nation. These National Identity Smart Cards offer the possibilities of electronic payment with the security of an identification card, as the holder’s picture is printed directly on the front. This was the broadest financial inclusion initiative ever in Africa, and plans are in place to expand financial access to 120 million in the near future.

The company is also working with agencies in Africa to bring banking to those who do not yet have banking accounts. The South African Social Security Agency (SASSA) and MasterCard have been working together to bring 15 million grants to 10 million recipients, helping spread banking access and resulting in $375 million saved in operational costs.

Financial Future

As it stands, 54 percent of South Africans have an account with a formal banking institution. While 80 percent of sub-Saharan Africa is unbanked, initiatives like the one between SASSA and MasterCard are looking to change that. As the burgeoning class of African consumers is spending more (an estimated $1 trillion in 2012), the financial sector is expected to keep pace, and should grow by a 40 percent margin by 2020. It’s no surprise, then, that when combined with the amazing cashless opportunities that are sweeping the continent, Africa will contain seven of 10 of the fasted growing economies in the world by 2015.

Mobile payments and credit cards will work hand-in-hand to give African’s the financial freedom to securely spend in these blossoming economies, both in online and in-person capacities. To align themselves with the bright outlook of these growth opportunities, smart companies will poise themselves to be prepared to accept these types of payments.

Eran Feinstein is the founder of Direct Pay Online, a global e-commerce and online payments solutions for the travel and related industries. With over 14 years of leading technology, sales, marketing and operation teams Eran is an authority in the East African e-commerce and payments arena. He’s also an avid marathon runner.